25C00100 - Entrepreneurship and Innovation Management, 01.11.2018-22.11.2018

This course space end date is set to 22.11.2018 Search Courses: 25C00100

Glossary

A | B | C | D | E | F | G | H | I | J | K | L | M | N | O | P | Q | R | S | T | U | V | W | X | Y | Z | ALL

O |

|---|

opportunity costOpportunity cost refers to the benefit that a person gave up by deciding to take a particular course of action. Because every resource (money, time, physical assets) can be put to alternative uses, every action carries an opportunity cost. This is an important consideration in decision making in business. You can find a more detailed explanation of the concept here: http://www.econlib.org/library/Enc/OpportunityCost.html | ||

P |

|---|

P=MCPrice equals marginal cost, meaning the price just

covers the cost of producing that unit of beer but selling that unit of beer

does not generate any profit. | ||

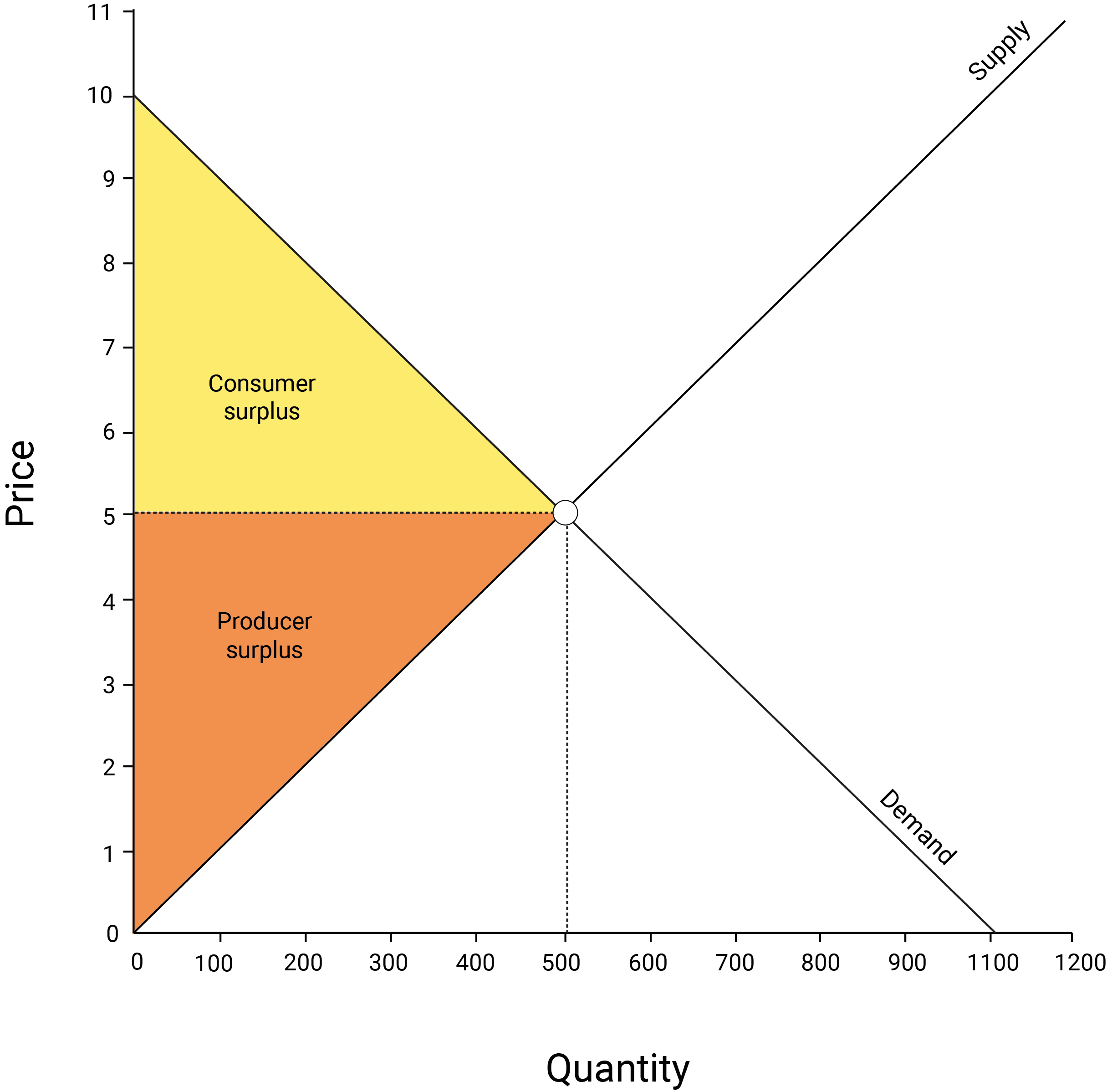

producer surplusProducer

surplus is the flip side of consumer surplus. It is defined as the difference

between the price (P) that the consumer pays for the product, and the cost (C)

to the firm of making that product. If P – C > 0, the firm is making money

and generating producer surplus.

| ||

R |

|---|

recoupWe could assume, for example, that Emma could resell her brewing equipment at exactly the same price that she originally bought them if she exited the business. We could also assume that she would not need to invest in advertising, which is typical sunk cost for a new business. | ||

S |

|---|

short runShort

run refers to a situation when one factor of production is held fixed. For

example, tank capacity in Jane’s brewery is fixed in the short run because

increasing it would require investments in further tanks, which she cannot do

immediately. However, she can make such investments in the long run. | ||

Supply curveSupply curve depicts the quantities that a producer is willing to supply for different prices. This curve is upward sloping: a producer is happy to supply more if the price is high. On a market level, this also means that when the price is high, there are more suppliers willing to operate in the market.

| ||

T |

|---|

transaction costPlease find an explanation about the transaction cost economic theory here. | ||

transaction costsIn a broader sense, transaction costs refer to the costs inherent in economic transactions that are not part of the price paid for a product or service. For example, many people would pay $3 for an ice-cream in a parlour 100 metres from their home, than drive 3 km to another parlour for the exact same ice-cream for $2. Why? Because the transaction cost of petrol, time and effort involved in driving those 3 km there and back are greater than the $1 saving in the price of the ice-cream. | ||

V |

|---|

value chain | ||